05/21/2026

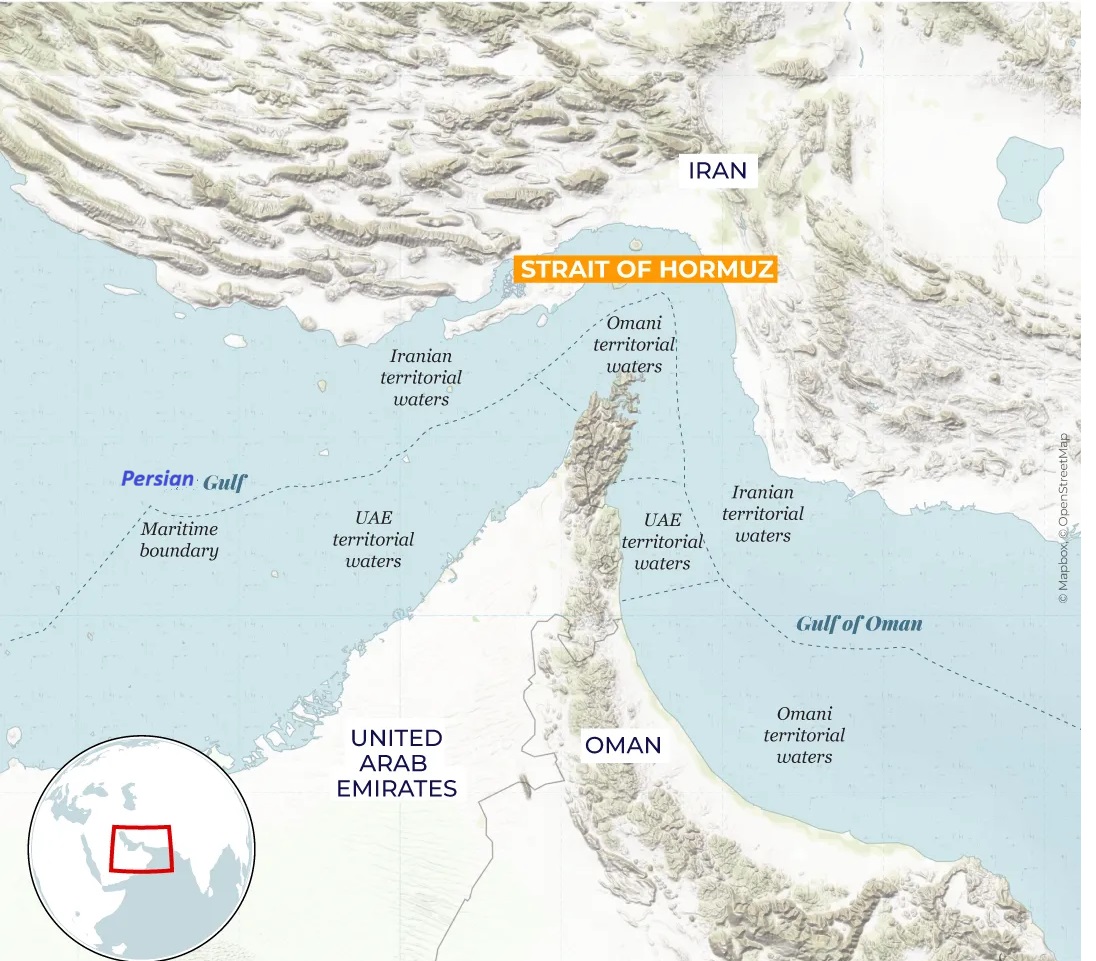

The Persian Gulf has always been one of the most sensitive regions for marine insurance because it combines three major risk factors: dense tanker traffic, strategic oil and gas exports, and repeated military tension around the Strait of Hormuz. When conflict rises in this region, ship insurance does not simply become more expensive; it can determine whether a vessel sails at all.

The current Strait of Hormuz crisis has again shown that insurance is one of the hidden control mechanisms of maritime trade. Even when cargo is available, ships are technically ready, and charterers want the voyage performed, the movement may stop if war-risk insurance becomes unavailable, unaffordable, or too uncertain. In May 2026, Reuters reported that traffic through the Strait of Hormuz had fallen from a normal average of about 125–140 vessels per day to around 10 vessels per day, with about 20,000 seafarers stranded on hundreds of ships. That collapse in traffic was driven not only by physical danger, but also by the insurance, liability, and risk-pricing consequences of war.

Why the Persian Gulf Is So Important for Marine Insurance

The Persian Gulf is not just another trading area. It is one of the world’s most important maritime energy corridors. Tankers carrying crude oil, refined products, LNG, LPG, chemicals, and petrochemicals pass through the Strait of Hormuz to reach global markets. When the strait becomes unsafe or politically restricted, the effect spreads across freight markets, oil prices, chartering decisions, port operations, and marine insurance.

For insurers, the region is difficult because the risk is not limited to normal navigation hazards. It includes missiles, drones, mines, military detention, seizure, terrorism, sabotage, sanctions exposure, cyber disruption, port closures, blocked routes, crew injury, pollution following an attack, and wreck removal after a casualty. This is why voyages into the Persian Gulf and through the Strait of Hormuz often require additional war-risk cover beyond ordinary hull and machinery insurance.

The Lloyd’s Market Association’s Joint War Committee maintains “Listed Areas” where vessels are considered exposed to increased war-related risks. Ships entering those areas may need additional war-risk cover, and the price is negotiated case by case by underwriters, brokers, shipowners, and charterers.

Historical Background: From the Tanker War to the Gulf War

The insurance sensitivity of the Persian Gulf did not begin in 2026. It has deep historical roots.

During the Iran–Iraq War, especially the so-called Tanker War of the 1980s, commercial vessels and oil tankers became direct targets. Both Iran and Iraq attacked merchant shipping connected to the other side’s oil exports. The Tanker War became one of the most serious attacks on commercial shipping since the Second World War, with hundreds of merchant ships damaged and significant loss of life among civilian seafarers.

This period shaped the modern understanding of war-risk insurance in the Persian Gulf. Insurers learned that commercial ships in the region could become strategic targets even if they were not naval vessels. A tanker could be attacked because of its flag, cargo, charterer, destination, ownership structure, or perceived political connection. This made insurance pricing more political and intelligence-driven.

The 1990–1991 Persian Gulf War again affected marine insurance. After Iraq’s invasion of Kuwait in August 1990, insurers increased war-risk rates for ships trading to Persian Gulf ports. According to the Strauss Center’s Strait of Hormuz insurance-market summary, cargo insurance rates later fell as the perceived risk of immediate war declined, but the crisis reinforced the idea that Persian Gulf war risk could rise or fall rapidly depending on military and diplomatic developments.

The historical lesson is clear: in the Persian Gulf, insurance markets respond quickly to war, but they also distinguish between different levels of exposure. A vessel calling at a lower-risk port may be priced differently from a tanker carrying strategic cargo through the Strait of Hormuz during active hostilities.

The Current Strait of Hormuz Crisis and Insurance Shock

The 2026 Strait of Hormuz crisis has produced one of the sharpest recent increases in maritime war-risk pricing. Reuters reported in March 2026 that maritime insurance premiums for war coverage were surging, in some cases by more than 1,000%, as the conflict widened and insurers rapidly repriced exposure in the Persian Gulf.

India’s response shows how serious the insurance problem became. Reuters reported in April 2026 that India was preparing a $1.5 billion sovereign guarantee fund for insurers, alongside a separate $300 million industry pool, because war-risk insurance premiums for Persian Gulf shipping had surged by up to 1,000% and the definition of risky zones had expanded beyond the Strait of Hormuz itself.

This is important because it shows that the crisis has affected not only shipowners, but also governments. States that rely on Persian Gulf energy imports may need to support insurance availability because private underwriters may either withdraw, restrict cover, or charge premiums so high that normal trade becomes economically impossible.

War-Risk Premiums: From Routine Cost to Voyage-Deciding Factor

War-risk insurance is usually calculated as a percentage of the vessel’s insured value for a specific voyage or period. When the region is calm, the premium may be relatively small compared with total voyage revenue. During crisis conditions, it can become one of the largest single voyage costs.

For example, Al Jazeera reported in March 2026 that war-risk premiums had risen as high as 1% of the value of a ship, compared with about 0.2% the previous week. For a tanker worth $100 million, that would mean a rise from roughly $200,000 to about $1 million for a single voyage.

Other market reporting suggested even higher figures for more exposed vessels. Lloyd’s List reported that seven-day war-risk cover in the Middle East Gulf region had risen roughly tenfold compared with levels before the U.S. and Israeli attack on Iran, with high-risk cases potentially reaching double-digit millions of dollars per voyage.

This kind of pricing changes the economics of shipping. A charterer may refuse to pay the additional premium. A shipowner may refuse the voyage because the crew and asset risk are too high. A cargo owner may delay shipment. A bank or financier may require proof of adequate cover before allowing the vessel to proceed. In practice, insurance becomes a gatekeeper of maritime movement.

Which Marine Insurance Covers Are Affected?

The Strait of Hormuz crisis affects several branches of marine insurance.

| Insurance category | How the crisis affects it |

|---|---|

| Hull and Machinery | Physical damage to the ship from missiles, drones, mines, explosions, or military action may be excluded from ordinary H&M and require war-risk cover. |

| War Hull | Premiums rise sharply for vessels entering listed or high-risk Persian Gulf areas. |

| P&I Insurance | Third-party liabilities remain critical, including crew injury, pollution, collision, wreck removal, and port damage. |

| War P&I | Covers liabilities arising from war perils, but pricing and availability depend on market capacity and reinsurance. |

| Cargo Insurance | Cargo owners may need war-risk extensions for oil, LNG, chemicals, vehicles, or containerized goods. |

| Loss of Hire | Owners may seek cover for income loss if a ship is delayed, detained, damaged, or unable to trade. |

| Kidnap, ransom, detention, and seizure | Relevant where ships may be boarded, detained, or used as leverage. |

| Political risk and sanctions cover | More important when payments, counterparties, or cargo interests involve sanctioned entities or territories. |

A Howden Re report on the Strait of Hormuz crisis explains that the affected insurance classes include War Hull Risk, War P&I, War Cargo Insurance, and environmental damage cover. It also notes that maritime insurers expanded high-risk zones across parts of the Persian Gulf and Gulf of Oman, triggering additional premiums and tighter insurance conditions.

Listed Areas and the Expansion of Risk Zones

One of the most important insurance developments in the current crisis has been the expansion of war-risk listed areas. When the Joint War Committee expands a listed area, the change does not automatically prohibit ships from sailing. However, it signals that underwriters consider the area to be exposed to increased war-related risk. This usually leads to additional premiums, stricter terms, shorter notice periods, or more detailed voyage declarations.

Safety4Sea reported in March 2026 that the Joint War Committee had expanded its listed areas, a move that typically results in higher additional premiums and more restrictive voyage terms for vessels entering or operating within the newly defined zones.

Industry guidance from marine insurers also indicated that the March 2026 changes included the Persian Gulf and Gulf of Oman, including the Strait of Hormuz, alongside other expanded areas.

The practical result is that the crisis has not been priced as a narrow “strait-only” risk. Underwriters increasingly view the wider Persian Gulf operating environment as exposed, because ships may be attacked, detained, delayed, inspected, or blocked before or after reaching the strait itself.

Insurance Availability Versus Safety Reality

A key point is that high premiums do not mean insurance has completely disappeared. The Lloyd’s Market Association stated in March 2026 that war insurance remained available in the Lloyd’s and London company market for vessels wishing to transit the Strait of Hormuz. It also noted that liability coverage through the P&I Clubs was non-cancellable and remained reinsured in the London market, although some fixed-premium P&I covers for charterers had been cancelled and repriced.

This distinction matters. The crisis is not simply “no insurance, no voyage.” In many cases, the market may still offer cover, but at a price and under conditions that shipowners or charterers consider unacceptable. Even when insurance is available, owners may still refuse to sail because of crew safety, vessel exposure, sanctions uncertainty, or the absence of reliable naval protection.

In other words, insurance availability does not automatically restore maritime traffic. A policy can compensate for financial loss, but it cannot fully protect seafarers from missiles, mines, detention, or death. This is why many owners remain cautious even when insurance can technically be purchased.

P&I Clubs and Liability Exposure

Protection and Indemnity insurance is especially important in the Persian Gulf crisis because a war-related incident can create enormous third-party liabilities. If a tanker is hit and spills oil, the incident may involve pollution claims, cleanup costs, cargo loss, crew injury, salvage, wreck removal, port closure, and damage to coastal infrastructure.

Ordinary P&I cover often excludes certain war risks, which are handled through separate war-risk arrangements. For shipowners, the key question is not only whether the vessel itself is insured, but whether liabilities arising from a war incident are covered. This is critical for tankers, LNG carriers, chemical tankers, and large container ships because a single casualty can generate liabilities far beyond the physical value of the ship.

The Strait of Hormuz crisis therefore increases concern over:

- pollution liability after missile or mine damage;

- crew injury and death claims;

- wreck removal in restricted waters;

- port and terminal damage;

- collision risk during convoy or congested navigation;

- salvage and general average disputes;

- liability if cargo cannot be delivered;

- disputes between owners, charterers, and cargo interests.

Cargo Insurance and Energy Trade

Cargo insurance has also been affected. Oil, LNG, petrochemicals, vehicles, fertilizers, and containerized cargoes may require additional war-risk cover when moving through the Persian Gulf. Cargo insurers price not only the route but also the cargo type, value, destination, ownership, and political exposure.

The disruption has already affected global trade. Reuters reported that Japanese auto exports to the Middle East plunged by more than 90% in April 2026 because war disrupted shipping routes and made transport difficult. This example shows that the insurance effect is not limited to tankers. Car carriers, container ships, bulk carriers, and general cargo vessels are also affected when underwriters price the entire region as high risk.

For energy cargoes, the consequences are even larger. If cargo insurance becomes too expensive or uncertain, oil and gas movements slow down. Buyers may seek alternative supply, sellers may delay liftings, and governments may intervene through guarantees or emergency reserves.

Reinsurance and Market Capacity

Behind the direct insurer stands the reinsurance market. Reinsurers absorb part of the risk from primary insurers. When conflict expands, reinsurers may tighten capacity, increase prices, or restrict the terms on which they support war-risk underwriters.

This is why a regional war can become a global insurance problem. A few major losses in the Persian Gulf could affect underwriting appetite far beyond the region. Reuters noted that reinsurers may tighten capacity as risks rise, which could further increase costs and reduce the availability of affordable cover.

If reinsurance capacity tightens, direct insurers become more selective. They may ask more questions about the ship’s ownership, flag, route, cargo, crew nationality, security arrangements, AIS behavior, sanctions exposure, and naval escort availability. The underwriting process becomes slower and more intelligence-driven.

Government Backstops and Sovereign Guarantees

When private insurance becomes too expensive or unstable, governments may step in. This is not new. During major wars, states have often provided war-risk insurance or reinsurance to keep strategic trade moving.

The 2026 Persian Gulf crisis has revived this logic. India’s reported plan for sovereign guarantees shows how importing states may support insurers to keep energy and cargo flows alive. The World Economic Forum also described how the Middle East war was pushing governments toward the role of “insurers of last resort,” as private markets suspended or repriced war-risk coverage for ships transiting the Strait of Hormuz and the wider Persian Gulf.

This changes the nature of marine insurance. It becomes not only a private commercial contract, but also a tool of economic security. Governments may decide that maintaining maritime flows is too important to leave entirely to private underwriters.

Charter Parties and Contractual Disputes

The crisis also affects charter-party relationships. When war-risk premiums rise, disputes may arise over who pays the additional premium: the shipowner, time charterer, voyage charterer, cargo owner, or buyer. The answer depends on the contract wording.

Common issues include:

- whether the Persian Gulf is a permitted trading area;

- whether the owner can refuse an unsafe port or unsafe route;

- whether the charterer must pay additional war-risk premium;

- whether delay caused by closure or detention counts as off-hire;

- whether deviation is permitted;

- whether force majeure applies;

- whether cargo delay gives rise to demurrage or damages.

War-risk clauses such as BIMCO-style clauses are designed for this type of situation, but disputes still arise because the facts change quickly. A route that was commercially acceptable when the charter party was signed may become high-risk before the ship arrives.

Sanctions Risk and Counterparty Screening

Insurance in the Persian Gulf crisis is also affected by sanctions risk. Underwriters must consider whether the vessel, owner, manager, charterer, cargo, bank, or payment channel has links to sanctioned entities. A ship may face different insurance treatment depending on its beneficial ownership, flag, cargo origin, destination, and political connection.

This means marine insurance is no longer only about physical danger. It is also about compliance. A vessel may be technically insurable from a war-risk perspective but still difficult to cover if sanctions exposure is unclear. Insurers may require enhanced due diligence, beneficial ownership checks, AIS records, route documentation, cargo documents, and declarations about counterparties.

Practical Effects on Shipowners

For shipowners, the Persian Gulf and Strait of Hormuz crisis has created several practical consequences.

First, voyage costs have increased sharply. Additional war-risk premiums can turn a profitable voyage into an unattractive one.

Second, insurance negotiations take longer. Brokers and underwriters may need updated route plans, vessel details, security assessments, and declarations.

Third, some owners may refuse Persian Gulf employment altogether, even if charterers are willing to pay premiums.

Fourth, vessels already trapped in the region may face insurance complications if policies expire, certificates need renewal, or the ship remains in a listed area longer than expected.

Fifth, banks and financiers may require confirmation of adequate insurance before allowing vessels to continue trading.

Practical Effects on Seafarers

Insurance is often discussed in financial terms, but it also affects crews. If a voyage is classified as high risk, seafarers may be entitled to special compensation, bonuses, or repatriation rights depending on contract terms, collective bargaining agreements, and flag-state rules.

The current crisis has placed thousands of seafarers under prolonged stress. Reuters reported around 20,000 seafarers stranded on hundreds of ships because of the sharp reduction in Hormuz traffic. Insurance may compensate owners for physical loss, but it does not remove the human risk. This is why many shipowners judge the voyage not only by premium cost but by the acceptability of exposing crews to danger.

How the Crisis Changes Underwriting Behaviour

The Persian Gulf crisis has made underwriters more selective. Instead of treating all ships equally, insurers are likely to differentiate between risk profiles.

A lower-risk vessel may be:

- non-U.S.-linked;

- non-Israeli-linked;

- not carrying strategic military-sensitive cargo;

- operated by a transparent owner;

- sailing under a reputable flag;

- using clear route reporting;

- supported by naval coordination or trusted security advice;

- free from sanctions complications.

A higher-risk vessel may be:

- linked to politically exposed owners or cargoes;

- carrying oil, LNG, military-sensitive goods, or strategic cargo;

- trading to or from sensitive ports;

- operating with unclear beneficial ownership;

- using suspicious AIS patterns;

- connected to sanctioned entities;

- unable to demonstrate proper war-risk and P&I arrangements.

This means premiums are no longer driven only by geography. They are also driven by identity, cargo, route, behaviour, and political perception.

Wider Market Effects

The insurance shock affects the wider maritime economy in several ways.

It raises freight rates because shipowners demand compensation for risk. It increases energy prices because oil and gas transport becomes more expensive and uncertain. It delays cargoes because ships wait for cover, naval advice, or safer passage. It reduces vessel availability because owners avoid the region. It shifts trade flows because buyers look for non-Persian Gulf sources. It encourages governments to consider sovereign insurance schemes. It may also accelerate investment in alternative routes, pipelines, storage, and regional supply-chain resilience.

In this sense, ship insurance becomes a transmission mechanism: local conflict in the Persian Gulf becomes global cost inflation through premiums, freight, cargo delay, and energy-market uncertainty.

Conclusion

The Persian Gulf War experience and the current Strait of Hormuz crisis both show that marine insurance is central to maritime security. During the Tanker War and the 1990–1991 Persian Gulf War, underwriters learned that merchant ships in the region could become strategic targets. In 2026, the same lesson has returned with greater complexity: missiles, drones, mines, sanctions, cyber risks, detention, crew safety, and reinsurance capacity now shape whether ships can move.

The current crisis has increased war-risk premiums, expanded listed areas, tightened underwriting conditions, complicated P&I and cargo insurance, and pushed some governments toward sovereign guarantee schemes. Although insurance may still be available in some markets, the cost and risk are often high enough to discourage voyages.

The most important lesson is that insurance is not a secondary financial detail. In the Persian Gulf and Strait of Hormuz, insurance is part of the maritime infrastructure itself. Without affordable and reliable cover, ships remain at anchor, cargoes remain delayed, crews remain exposed, and global trade becomes vulnerable to a narrow but strategically decisive waterway.